For the past few years, one phrase has dominated housing market conversations: the mortgage rate lock-in effect.

Millions of homeowners secured ultra-low mortgage rates below 3% during the pandemic, creating a powerful disincentive to sell. Why give up a once-in-a-lifetime rate and trade it for something double—or more? The result was predictable: fewer listings, tighter inventory, and a market that felt frozen in place.

But as we head into 2026, something important has changed.

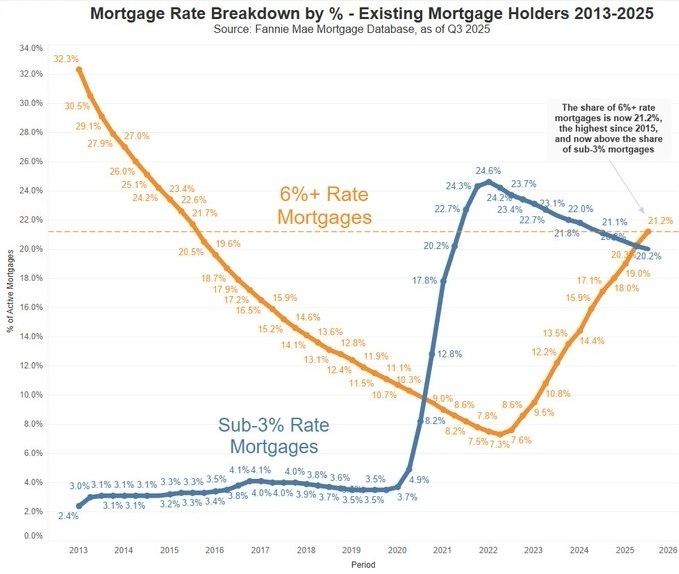

For the first time, there are now more homeowners with mortgage rates above 6% than those with rates below 3%. That shift marks a quiet but meaningful turning point for housing supply.

A Changing Rate Landscape

As of the end of 2025, 21.2% of outstanding mortgages carry rates above 6%, the highest share since 2015—and nearly three times higher than the pandemic-era low.

This didn’t happen overnight, and it didn’t require a booming housing market to get here.

Even in today’s slower environment for home sales and refinances, roughly 5–6 million Americans take out a new mortgage every year. Over the past few years, nearly all of those loans have been originated at rates north of 6%. Each year, that adds another cohort of homeowners whose payments and rates are far closer to current market levels.

Over time, that accumulation matters.

Why This Weakens the Lock-In Effect

The lock-in effect was strongest when the gap between existing mortgage rates and market rates was extreme. A homeowner with a 2.75% mortgage faced a massive financial penalty to move.

But homeowners with rates at—or near—today’s levels don’t face that same psychological or financial barrier.

When your mortgage rate already starts with a “6,” the cost of moving feels far more manageable. The decision becomes less about preserving a historically low rate and more about life factors: job changes, growing families, downsizing, relocation, or upgrading homes.

In short: when rates feel “normal,” mobility returns.

Why This Is Actually Good News

At first glance, rising rates and higher-rate mortgages may sound negative. But from a market health perspective, this shift is constructive.

As more homeowners hold mortgages closer to market rates:

- More sellers are likely to enter the market

- Listing activity should gradually increase

- Inventory pressure should ease over time

- Price discovery becomes healthier and more balanced

This doesn’t mean a sudden flood of homes or a sharp market correction. Housing supply tends to adjust slowly. But it does mean that the artificial constraint caused by ultra-low legacy rates is beginning to loosen.

What to Expect Going Forward

The fading lock-in effect won’t dominate headlines the way rate cuts or affordability debates do—but its impact will quietly build year after year.

As higher-rate mortgages continue to replace ultra-low ones, the housing market gains flexibility. Buyers get more options. Sellers regain motivation. And professionals across real estate and mortgage see a more functional, less gridlocked market.

In other words, while rates may remain elevated compared to the pandemic era, the market itself is becoming less stuck.

And that’s a meaningful step toward a healthier housing ecosystem in the years ahead.